WHAT IS A HELOC

A Home Equity Line of Credit (HELOC) is a type of loan that functions similar to a credit card, allowing you to withdraw funds when you need them, up to your approved credit limit.

Monthly interest and payments only begin to accumulate once have have removed funds. A bank will lend funds using the equity in your property as collateral for the loan. Equity is the difference between the current value of your home and the balance of your mortgage. For example if your home is valued at $100,000 and you owe $80,000, then you have $20,000 in equity.

When should I use a HELOC

There are many situations where you can take advantage of a HELOC however, there are also situation where you should NOT use HELOC funds.

Before you decide to use HELOC funds, make sure the following statements are true:

1. My monthly income is stable and consistently greater than my monthly expenses.

2. My debt is minimal and under control.

3. I have money set aside to afford the upfront fees to open and maintain a HELOC.

- Capital improvements

- Real estate investments

- Education

- Private lending

- Business loans

- Debt consolidations

- Emergency funds (Medical/Unemployment)

- Luxury Items

- Cars, boats, motorcycles, RVs (depreciable assets)

- Vacations

- Weddings

- General Bills and expenses

Loan to Value

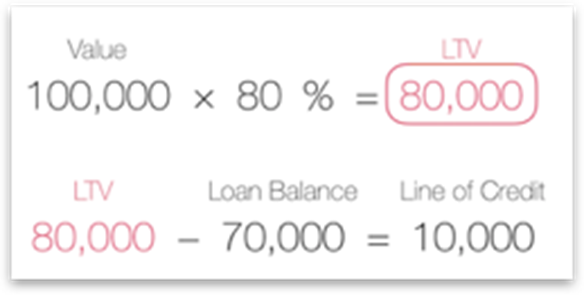

To protect their investments, most lenders require that the borrower maintain a certain amount of equity in the property. This buffer is commonly referred to as equity, expressed as loan to value, or LTV.

Loan to value (LTV) is the ratio between the loan amount and the value of the property. Banks lend between 65-100% LTV.

If a bank states they will loan 80% LTV, it means they will allow you to secure a line of credit on your existing equity up to 80% of the value of the property.

Using our previous example, if you house is valued at $100,000 and you owe $80,000, then you have a loan to value ratio of 80%, leaving no additional equity to loan against.

If that same mortgage was $70,000, you could borrow $10,000, leaving $20,000 or 80% LTV.

NOTE: Even though some lenders will loan more than 80% LTV, it is not recommended. Given that HELOCs are secured against the underlying property, failure to repay the loan may result in foreclosure.

Loan Terms and Qualifications

Banks consider the follow factors when underwriting HELOCs:

Property value

Equity

Personal credit score

Debt to income ratio

Employment history

The loan will most often have a variable rate based on the applicants credit score and current prime rates.

Most banks will lend between 80-100% LTV on your primary residence and 65-75% on non-owner occupied properties.

Calculating Interest

HELOC rates are tied to the prime rate, as of this publication rates are 3.25 %. The variable HELOC interest payments change monthly in association with the prime rate.

Standard mortgages use compound daily interest plus principle, whereas HELOCs use annualized interest-only payments (Adjusted monthly). HELOCs typically have a periodic adjustment cap. The maximum total interest charges are capped at 16% in North Carolina and 18% in the other states.

The formula for calculating 6% is .06 divided by 365 or .000164, which is multiplied by the average daily balance during the month. The interest on $100,000 is $16.44 per day and $509.64 per month.

Draws

The loan will be generated for a certain amount based on the available equity in the property. The rate will be based on the current prime rate and the borrowers credit score.

HELOCS have a draw period, during which the borrower can use the line of credit, and a repayment period during which the loan must be repaid. The draw period is typically 10 years and the repayment period is usually 10-20 years.

Repayment

During the draw period borrowers are only required to make interest payments. The full balance is due at the end of the draw period as a lump sum balloon payment. In many cases you can apply to extend the line of credit for another fixed term, or roll the principle balance into a fixed second mortgage.

Interview Lenders

Take the time to interview several lenders. HELOC programs can vary significantly. I found that smaller banks and credit unions have the best programs.

Here is a list of questions you can use when interviewing potential banks and lenders.

1. What are the different HELOC products offered by your company?